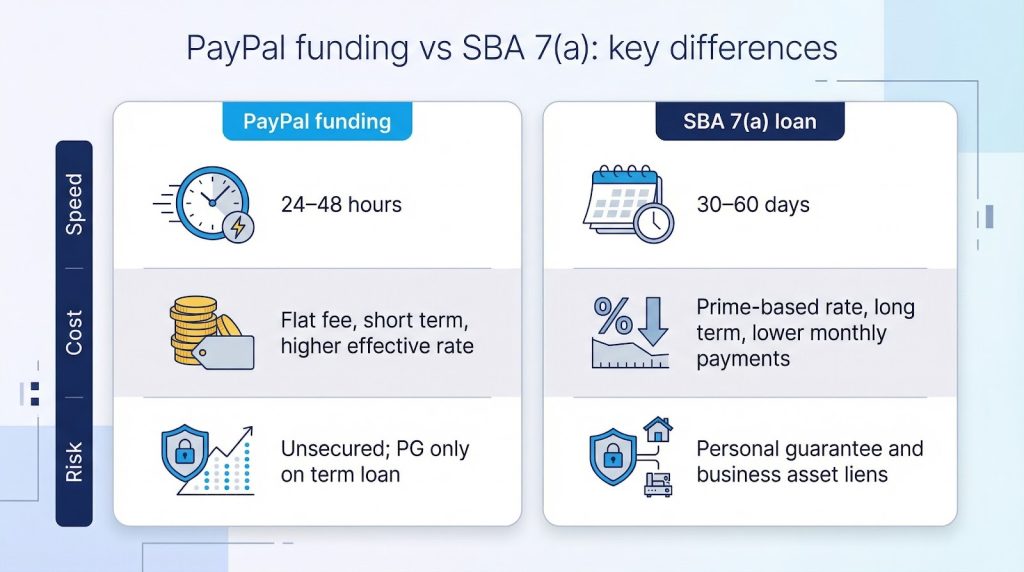

Two options dominate the search. PayPal can drop Working Capital or LoanBuilder funds into your account within one business day. The SBA 7(a) program swaps speed for lower rates and ten-year terms—but asks for paperwork and banker sign-off.

Which door opens wider for you? This guide unpacks eligibility, timing, cost, and risk so you can decide with confidence.

Table of Contents

Table of Contents

Key differences at a glance

Picture two very different runways.

The PayPal lane is short and brightly lit. You answer a handful of online questions, the algorithm scans nine months of revenue history and, if you clear roughly $33,000 a year, it can push up to $150,000 into your bank account as soon as the next business day (see the Business Credit Workshop analysis).

The SBA lane is a long, well-paved strip laid out by bankers and the federal government. It funds everything from a $50,000 working-capital boost to a $5 million expansion, but only after you prove you are a qualifying U.S. small business and hand over tax returns, financials, and a personal guarantee, according to the U.S. Small Business Administration.

Speed is the first contrast. PayPal money can appear within 24–48 hours. SBA money often arrives 30–60 days after your initial application because lenders underwrite manually and the agency still has to issue a guarantee number.

Cost is the second divider. PayPal charges one fixed fee that you repay over 13–52 weeks. That simplicity hides an effective interest rate well above traditional bank territory. SBA loans cap rates a few points above Prime and stretch payments out five to ten years, lowering the monthly bite even on six-figure balances.

Finally, consider risk. PayPal requires no collateral; SBA lenders file liens on business assets and expect a personal guarantee from every owner with at least twenty percent stake. PayPal bets on your future sales, while the SBA asks you to pledge the farm if you own one.

Keep these contrasts in mind as we dive deeper into each option. They frame every decision that follows.

PayPal financing: what it takes to qualify

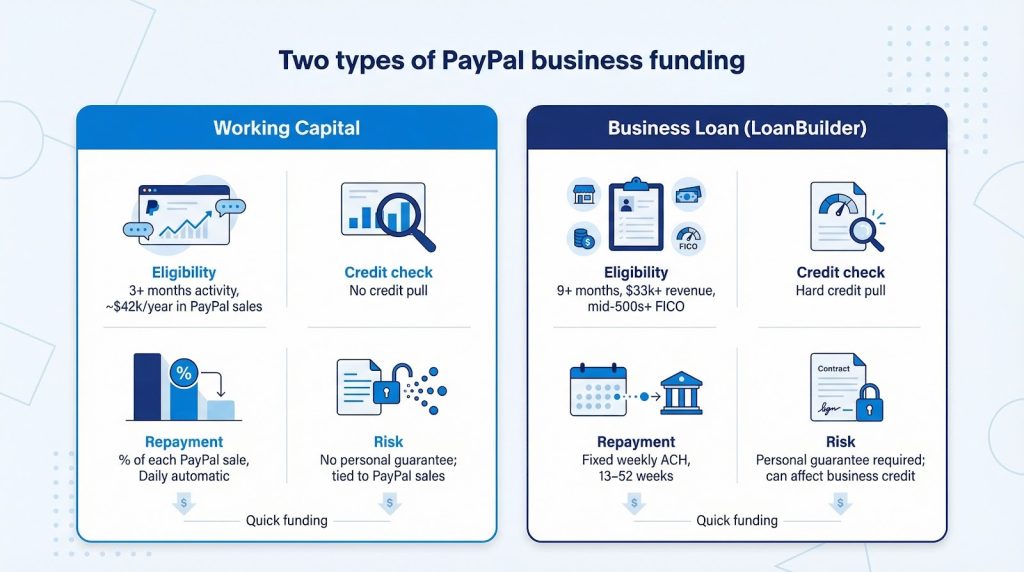

PayPal Working Capital – sales power turned into fast cash

Working Capital feels like an advance on tomorrow’s PayPal sales. You skip credit-score boxes, tax returns, and collateral. PayPal’s algorithm reviews the revenue already running through your account.

If your Business or Premier account shows at least three months of activity and about $42,000 in annual PayPal sales, an offer can appear inside your dashboard. The amount tops out at roughly 35 percent of your trailing-twelve-month sales, so a merchant processing $120,000 a year may see about $40,000. Approval is instant because PayPal already holds the data a bank would chase for weeks.

Paperwork is light. You confirm legal name, business address, and the percentage of each future sale you want to allocate to repayment. Click “Accept,” and funds usually settle in your PayPal balance or linked bank account the next business day.

The trade-off for speed is cost and control. PayPal charges a single fee—similar to prepaid interest—that varies with risk and the repayment percentage you choose. Select a 20 percent sweep from every sale and the fee stays modest; choose 10 percent and the fee rises because PayPal waits longer to recover principal.

Repayment is automatic. Busy days repay more, slow days less. You must still clear at least 10 percent of the original balance every 90 days; fall short and PayPal initiates catch-up withdrawals.

No credit pull means no boost to your score for paying on time, but also no ding for applying. Defaults stay mostly inside PayPal’s system: the company can freeze incoming payments or send the balance to collections, yet your personal credit report remains untouched.

For sellers who rely on PayPal and prize speed, Working Capital can be a practical cash source. Just keep sales flowing, or the door closes.

PayPal Business Loan – term financing with a personal guarantee

LoanBuilder, marketed as the PayPal Business Loan, promises similar speed but targets owners who need a lump sum with a fixed weekly schedule.

Start with the online questionnaire. It asks for time in business, annual revenue, and personal credit score. Meet the minimums—about nine months in operation, $33,000 in revenue, and a FICO in the mid-500s—and the system shows pre-qualified terms within minutes, according to Business Credit Workshop.

Here comes the first major fork from Working Capital: PayPal runs a hard credit pull once you choose an offer. That inquiry may lower your score a few points, and approval depends on a brief review of your bank statements. Many borrowers see final sign-off the same day.

Cash remains quick. Sign the e-documents before noon, and WebBank—PayPal’s partner lender—often wires funds to your business account by the next business day.

Terms range from 13 to 52 weeks. Each option displays the exact total payback, a flat dollar fee rather than an interest rate. Shorter terms carry lighter fees; stretching to a full year costs more.

Unlike Working Capital, LoanBuilder requires a personal guarantee. The loan is unsecured, but you pledge to repay if the company falls behind. Miss a weekly debit and PayPal can pursue collections through standard legal channels, and the default appears on your business credit report.

Because repayment is fixed, it never shrinks during a slow week. Predictability helps if revenue is steady, yet it can pinch during a slump. Treat it as bridge money—fuel for marketing or inventory—rather than a long-term anchor.

SBA 7(a) loans: core eligibility criteria

The SBA 7(a) program looks friendly at first glance—low rates, ten-year terms, up to $5 million—yet lenders still put borrowers through a tight checklist before releasing funds. Let’s walk through that list so you know, line by line, whether the door stays open.

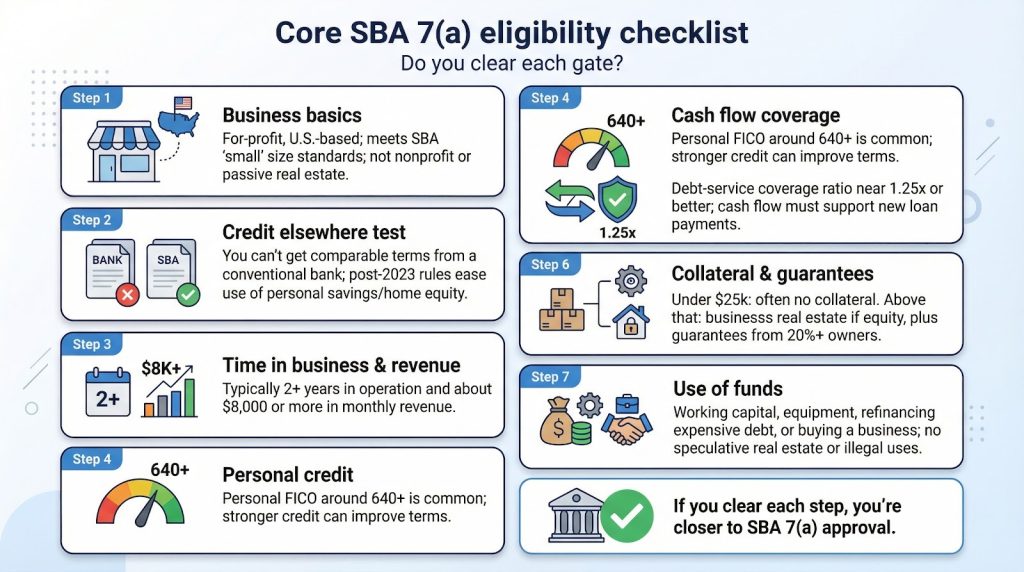

First, your business must be eligible. The SBA backs loans for firms that are for-profit, operate inside the United States, and meet size standards that define “small” in your industry. Nonprofits, passive real-estate investors, and gambling operations with more than a token share of revenue remain off limits, according to the SBA.

Next comes the “credit elsewhere” test. You sign a form stating you cannot secure comparable terms from a conventional bank. In August 2023 the SBA relaxed this rule, telling lenders they no longer have to count an owner’s personal savings or home equity before declaring that the business lacks reasonable credit, the Associated Press reported.

Now the hard metrics. Marketplace data from Lendio shows most lenders start around two years in business, at least $8,000 in monthly revenue, and a personal FICO of 640 for their SBA loans.

They also calculate a debt-service-coverage ratio; expect them to require that your cash flow covers new loan payments by at least 25 percent. Some mission-driven or online SBA lenders will accept thinner files, but the trade-off is extra scrutiny or higher spreads.

Collateral matters, though lack of it is not fatal. Loans under $25,000 need no pledged assets. Above that, the lender secures what it can—inventory, equipment, accounts receivable—and, for balances over $350,000, a lien on personal real estate if equity exists. Regardless of collateral, every owner with 20 percent or more of the company signs a personal guarantee. Miss payments and the government can collect just like a private creditor.

Finally, your use of funds must be eligible. Working capital, equipment, refinancing expensive debt, even buying a business qualify. Pure investments, speculative real estate, and anything illegal do not.

Submit one short form, and you usually learn within 24 hours whether your credit profile and cash flow meet current 7(a) cutoffs.

Lendio’s dedicated SBA team then aims to close small 7(a) loans in under 30 days—sometimes as fast as two weeks—by routing that pre-packaged file to lenders already familiar with its standardized format, a process that has helped the platform facilitate more than $15 billion in funding for over 400,000 small businesses.

Pass those gates and you have a solid chance of tapping the most affordable long-term capital on the small-business market.

SBA paperwork and the real-world timeline

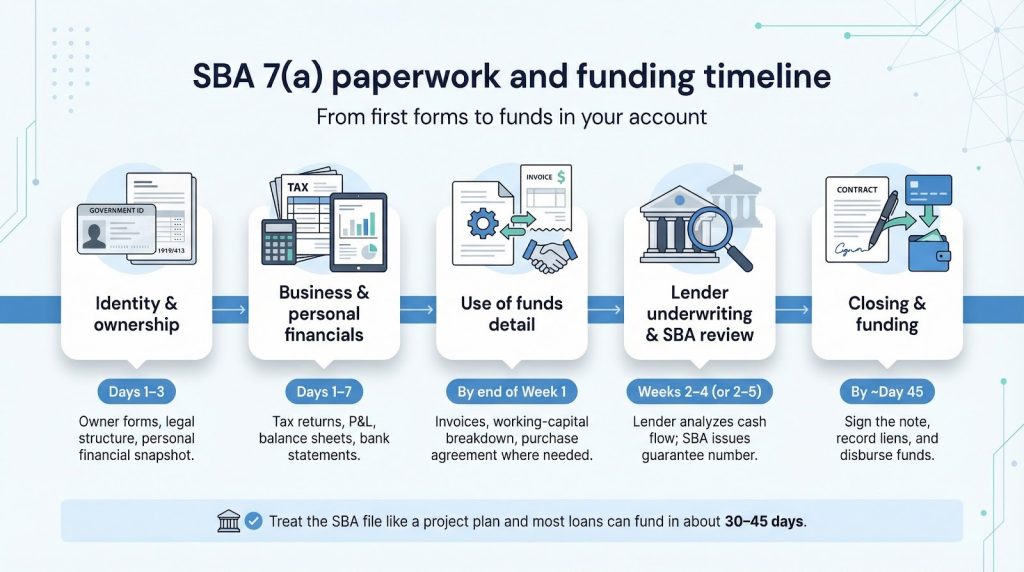

Paperwork is the toll you pay for low-cost capital. The stack feels endless, yet every page answers one of three lender questions: Who are you, how healthy is the business, and what will you do with the money?

Start with identity. Complete SBA Form 1919 for each owner and Form 413 for personal financial statements. These prove ownership percentages, legal status, and net worth.

Financial health comes next. Prepare the last two or three years of business tax returns, profit-and-loss statements, and balance sheets. Lenders match those numbers against recent bank statements to confirm cash really flows the way the tax forms claim. They also review your personal tax returns to gauge global income, because you—not just the company—guarantee repayment.

Use of funds rounds out the file. Supply invoices for equipment, a breakdown of working-capital needs, or a signed purchase agreement when buying a business. Lenders plug those figures into their model and upload the package through the SBA portal for a guarantee number.

Gathering documents usually takes a disciplined owner one week. Lender underwriting and SBA sign-off add another three to five weeks, depending on how fast you answer follow-up questions. Closing then slides in at the finish line: signing the note, recording liens, and funding, often within 45 days when everyone stays responsive.

Treat the checklist like a project plan rather than a burden, and the timeline shrinks.

Speed to cash: 24 hours or 45 days?

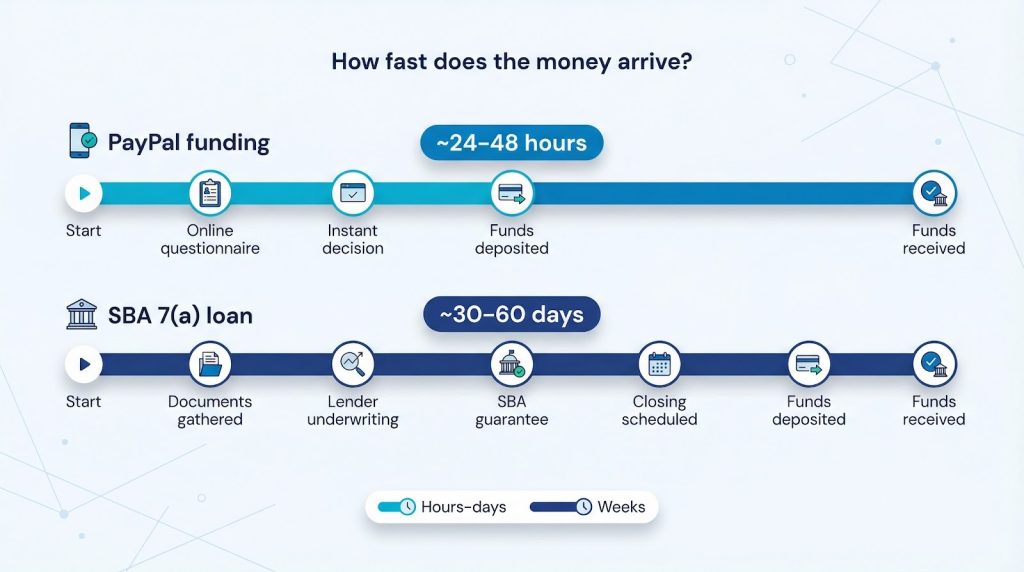

Funding speed marks the clearest gap between these two paths.

With PayPal, application and approval almost blend together. Working Capital uses data already in your account, so an offer can appear as soon as you finish the form. Sign electronically, and the money usually settles in your PayPal balance or linked bank account the next business day. LoanBuilder is similar: complete the questionnaire in the morning, clear a quick credit check by lunch, and WebBank can wire funds within 24–48 hours, according to Business Credit Workshop.

SBA money moves more slowly. Even a prepared borrower spends about one week gathering documents, another two to three weeks in lender underwriting, and then waits while the SBA issues its guarantee number and the bank schedules closing. Most real-world closings land 30–60 days after you press “submit,” and anything faster is rare.

If payroll is due Friday and cash is tight, PayPal wins on speed. If you are planning a spring expansion and can wait a month, the time you invest in an SBA loan often pays off through lower costs and longer terms.

Cost of capital: PayPal’s fixed-fee reality

PayPal keeps pricing simple. You borrow a set amount and agree to repay that amount plus one all-inclusive fee. No interest mounts daily, and no surprise charges appear later.

For Working Capital, the fee depends on two levers: the share of each PayPal sale you pledge toward repayment and PayPal’s internal risk score. Choose a 20 percent sweep from every sale and the loan clears faster, so PayPal discounts the fee. Pick a 10 percent sweep and the company charges more because it waits longer to recover principal. Either way, the fee locks on day one; repay tomorrow or next year, you owe the same total.

LoanBuilder follows the same flat-fee idea but ties price to your credit file and term length. A 13-week schedule costs less than a 52-week plan. PayPal shows the exact total payback before you sign, so there is no guessing. Independent reviewers place effective annual rates in the mid-teens to low-30s, cheaper than many merchant cash advances yet higher than bank pricing.

Repayment mechanics shape cash flow more than interest tables. Working Capital pulls a slice of revenue daily. Strong sales speed payoff but raise the implied APR because the flat fee spreads over fewer days. LoanBuilder debits a fixed weekly ACH, so owners must budget the payment even in slow weeks.

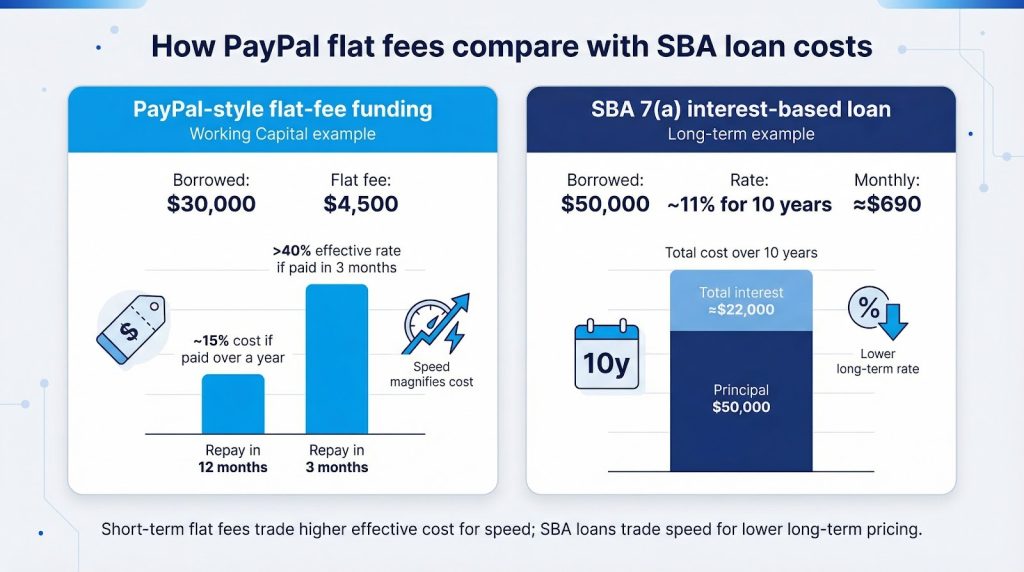

The math is blunt. A $30,000 Working Capital advance with a $4,500 fee equals a 15 percent cost if you take a full year to repay, but the rate climbs past 40 percent when brisk holiday sales clear the balance in three months. PayPal’s speed and convenience carry a premium; the quicker you repay, the higher that premium feels in percentage terms.

In short, PayPal financing works like prepaid interest. It is clear, quick, and easy to forecast, yet expensive once you compare it with traditional loans.

SBA loan costs and payment math

SBA pricing follows a classic formula: interest accrues, payments land once a month, and every charge is spelled out in writing. The blend of capped rates and long terms keeps the real burden lighter than many owners expect.

Start with interest. The SBA lets lenders charge Prime plus a spread that tops out at 2.75 percentage points for most 7(a) loans. With Prime near 8.5 percent in early 2026, many borrowers lock in rates just under 11.25 percent—about one-third the effective cost of a quick PayPal loan. Strong credit or larger balances can trim the spread further, pushing rates toward single digits, according to the SBA.

Fees come next. Loans under $500,000 carry no upfront guarantee fee through the current fiscal year. Balances above that pay up to 3.5 percent of the guaranteed portion. Lenders may also add a packaging fee capped at $2,500, a cost many owners roll into the loan rather than writing a separate check.

Now translate the pieces into dollars. Borrow $50,000 at 11 percent for ten years and the monthly payment lands near $690. Only about $460 of that amount counts as interest during the first year. Ride the full decade and total interest reaches roughly $22,000, yet the payment stays a predictable $690 every month.

Prepayment rules help, too. Because the term is under 15 years, you can retire the balance early with no penalty, a handy option if you sell the business or refinance later at a lower rate.

Overall, SBA funding trades speed for savings. Owners willing to wait a few weeks often save thousands over the life of the loan compared with fast-cash alternatives.

Collateral, guarantees, and personal risk

Collateral is where theoretical risk turns tangible.

PayPal keeps requirements light. Working Capital is unsecured and carries no personal guarantee; PayPal’s only hold is the stream of future PayPal sales. LoanBuilder does require a personal guarantee. No hard collateral changes hands, yet you promise to repay if the business falls behind. Miss a weekly debit, and PayPal may pursue collections through regular legal channels, and the default appears on your business credit report.

The SBA takes an opposite stance. Every owner with at least 20 percent equity signs a full personal guarantee, and lenders claim business assets when available. Borrow more than $25,000 and expect a blanket lien on inventory, equipment, and receivables. Pass $350,000, and the bank also secures any real estate equity you hold, even if that means a second mortgage on your home, according to the SBA.

That guarantee carries real consequences. If the loan defaults, the SBA reimburses the lender for up to 75 percent of the loss, then turns to you to collect. Treasury offsets, wage garnishment, and property liens can all follow until the balance is cleared. Defaulting on a PayPal loan mostly dents a credit report, while defaulting on an SBA loan can cost property.

Owners who prize asset protection or face volatile sales often choose PayPal despite the higher price. Those confident in steady cash flow accept the collateral drag because the savings can outweigh the risk.

Fast money rarely comes without strings, and slow money ties those strings to your assets. Pick the option that lets you sleep at night.

Pros and cons at a glance

PayPal financing

Pros

- Approvals in minutes, cash in a day.

- Minimal paperwork and no collateral.

- Flexible Working Capital repayments that rise and fall with sales.

Cons

- Flat fees translate into high effective interest, especially if you repay fast.

- Loan amounts cap around $150,000.

- Algorithmic approvals can vanish if sales dip, or if you leave the PayPal platform.

SBA 7(a) loans

Pros

- Prime-based rates, among the lowest in small-business finance.

- Terms up to ten years for working capital, and 25 years for real estate, producing small monthly payments.

- Borrow up to $5 million, and build a bank relationship along the way.

Cons

- Document-heavy application and a one- to two-month funding timeline.

- Personal guarantees and asset liens increase personal risk.

- Credit and cash-flow hurdles shut out very young or struggling firms.

Conclusion: Which option favors you?

Every business sits somewhere on the triangle of speed, cost, and risk. Let’s test a few real-world scenarios so you can see where you fit.

Picture a one-year-old e-commerce shop with $45,000 in annual PayPal sales. A container of holiday inventory will sell out in weeks, but the supplier wants payment tomorrow. The SBA will not help; the firm is too new and too small. PayPal Working Capital drops $20,000 into the account overnight. Inventory moves, the fee is paid, and the owner meets demand. Verdict: PayPal wins because timing matters more than price.

Now imagine a five-year-old landscaping company with $800,000 in revenue and a 690 credit score. Two new trucks must arrive before spring, and delivery can wait a month. The bank’s SBA channel offers a $200,000, seven-year loan at Prime plus two. Monthly payments land under $3,000, and the trucks themselves secure part of the note. PayPal cannot lend that much or that long. Verdict: SBA wins because price and term beat instant cash.

Third case: a boutique agency with uneven revenue. The business qualifies for an SBA loan, yet a fixed monthly payment feels risky during slow quarters. PayPal LoanBuilder offers $50,000 for one year at an $8,000 flat fee. The owner takes a smaller $25,000 slice, funds a marketing push, then plans to apply for SBA Express once cash flow steadies. Verdict: hybrid path; use PayPal as a bridge, then refinance with SBA when paperwork is manageable.

In short, choose PayPal when urgency or credit limits outweigh cost. Choose SBA when stable operations and planning time let you secure the cheapest money. You can start with one and shift to the other as needs change.